Chapter 10

In Chapter 9, we explored the Black-Scholes-Merton equation. It taught us that an option’s theoretical price is determined by a specific set of variables: the stock price, the strike price, time to expiration, interest rates, and implied volatility.

But as you know from looking at any financial news screen, these variables do not stand still. The stock price ticks up and down every microsecond. Time marches relentlessly forward. Implied volatility violently spikes during panic and collapses during calm.

Because the inputs are constantly moving, the price of your option is constantly moving.

If you manage a multi-million-dollar derivatives portfolio, you cannot just stare at the screen and guess how much money you will lose if the market drops 5% tomorrow. You need exact, quantifiable metrics that measure your portfolio’s sensitivity to each moving variable.

Enter The Greeks.

The Greeks are the dashboard of your financial vehicle. Just like a car’s dashboard has a speedometer, a tachometer, and a fuel gauge, a trader’s screen has Delta, Gamma, Theta, and Vega. In this chapter, we will focus on the two Greeks tied directly to the physical movement of the underlying stock: Delta and Gamma.

10.1 Introduction to the Dashboard

Before we isolate them, let’s briefly introduce the main dashboard. Each Greek measures the option’s sensitivity to one specific variable, assuming all other variables remain perfectly frozen.

- Delta (Δ): Sensitivity to the Stock Price. (Speed)

- Gamma (Γ): Sensitivity to Delta. (Acceleration)

- Theta (Θ): Sensitivity to Time. (Fuel Decay)

- Vega (ν): Sensitivity to Implied Volatility. (Fear/Uncertainty)

- Rho (ρ): Sensitivity to Interest Rates. (Macro environment)

By reading these metrics together, a trader can instantly map their multidimensional risk. Let’s dive deep into the first two.

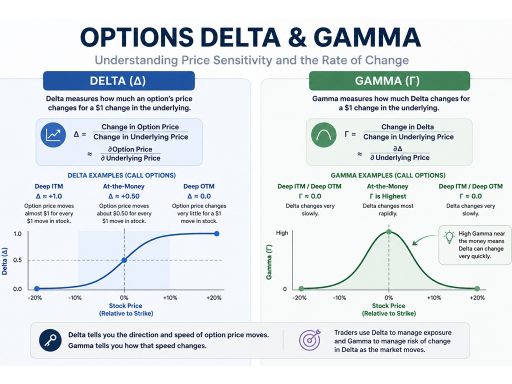

10.2 Delta (Δ): Speed and Probability

Delta is the most important Greek. It answers a very simple question: “If the underlying stock price goes up by exactly $1.00, how much will my option’s theoretical price change?”

- Call Options have a Delta ranging from 0 to 1.00. (Because Calls gain value when the stock rises).

- Put Options have a Delta ranging from -1.00 to 0. (Because Puts lose value when the stock rises).

If you own a Call option with a Delta of 0.50, and the stock goes up by $1.00, your option price will increase by 50 cents. If the stock drops by $1.00, your option will lose 50 cents.

The Three Faces of Delta

On the trading floor, Delta is used in three distinct ways:

1. Price Sensitivity (The Speedometer)

As we just defined, it is the expected dollar change in the option premium. Deep In-The-Money (ITM) options behave almost exactly like the stock itself; they have Deltas very close to 1.00 (or -1.00 for Puts). Far Out-Of-The-Money (OTM) options barely react to small stock movements; they have Deltas close to 0.

2. The Hedge Ratio

Think back to Chapter 7 and the Binomial Tree. To build our Replicating Portfolio, we had to buy a specific fractional amount of shares. That fraction is Delta.

If a market maker sells you a Call option, they are exposed to massive risk if the stock rallies. To hedge themselves perfectly, they look at the option’s Delta. If the Delta is 0.40, the market maker will immediately buy 40 shares of the underlying stock. This perfectly insulates them from the next microscopic tick of the stock price. We call this being Delta-Neutral.

3. The Probability Proxy

This is a trader’s mental shortcut. While not mathematically flawless, Delta serves as a highly accurate proxy for the probability that the option will expire In-The-Money.

- An option with a 0.80 Delta has roughly an 80% chance of expiring In-The-Money.

- An At-The-Money (ATM) option has a Delta of roughly 0.50 (a 50/50 coin flip).

- An option with a 0.05 Delta is a massive longshot; it only has a 5% chance of paying out.

10.3 Gamma (Γ): The Convexity Risk

If Delta is your speedometer, telling you how fast your option price is moving right now, Gamma is your accelerator.

Gamma measures the rate of change of Delta. It answers the question: “If the stock goes up by $1.00, how much will my Delta change?”

Why does this matter? Because Delta is not static! Remember our multi-period binomial tree in Chapter 8? As the stock price moved up, our required hedge ratio (Delta) increased from 0.525 to 0.95. That rate of change, that acceleration of Delta, is Gamma.

Gamma is always a positive number for option buyers (Long Gamma), and a negative number for option sellers (Short Gamma).

The Danger of Gamma for Market Makers

Imagine you are a market maker. You sold 100 Call contracts to a client. The options have a Delta of 0.50 and a Gamma of 0.10.

Because you sold 100 contracts (representing 10,000 shares), your total portfolio Delta is -5,000. You are short Delta.

To hedge this and become Delta-Neutral, you immediately buy 5,000 shares of stock. You take a breath. You are perfectly hedged. Your Net Delta is 0.

But then, the stock spikes by $1.00.

What happens?

- Because of Gamma, your option’s Delta changes. The Delta increases from 0.50 to 0.60 (0.50 original Delta + 0.10 Gamma).

- Your 100 short Call contracts now represent a short position of 6,000 shares.

- But you only own 5,000 shares in your hedge!

Because of Gamma, your perfect hedge instantly broke. You are now exposed. To get back to Delta-Neutral, you must frantically enter the market and buy 1,000 more shares.

And here is the painful part: because the stock just went up, you are being forced to buy those 1,000 shares at a higher price. If the stock then drops, your Gamma will reduce your Delta, and you will be forced to sell shares at a lower price.

Being Short Gamma forces a trader to constantly buy high and sell low just to stay hedged. It is a gruelling, expensive, and stressful position. This is the hidden cost of selling options!

The Beauty of Long Gamma

Conversely, if you buy options, you are Long Gamma.

If the stock rallies, your Delta increases, meaning your option accelerates its gains. If the stock drops, your Delta decreases, meaning your option decelerates its losses. Long Gamma is the mathematical essence of “Convexity.” It is the privilege of letting your winners run and cutting your losers short, built right into the math.

Note: Gamma is highest for options that are exactly At-The-Money (ATM) and close to expiration. An ATM option is standing right on the cliff’s edge; one small step by the stock dictates whether the option finishes ITM (Delta = 1) or OTM (Delta = 0). Therefore, its Delta is highly sensitive and changes violently (High Gamma).

10.4 Delta-Gamma Hedging in Practice

Let’s bring this together into a real trading floor scenario.

A large investment bank’s trading desk holds thousands of long and short options across dozens of different strike prices and expiration dates. Their computer systems instantly aggregate all these positions and spit out two numbers: the Net Portfolio Delta and the Net Portfolio Gamma.

Step 1: Delta-Neutrality (The First Line of Defense)

The desk’s primary mandate is almost always to be Delta-Neutral. If their Net Portfolio Delta is +10,000 (meaning they make money if the market rises and lose if it falls), the algorithmic trading system will automatically short 10,000 shares of the underlying stock to bring the Net Delta to exactly 0.

Step 2: The Gamma Problem

But as we just learned, if the portfolio has a massive Net Gamma (either positive or negative), that Delta-Neutral state will shatter the second the stock ticks.

- If you only hedge Delta, you are only protected against infinitesimally small stock movements.

- If the market gaps open 5% lower due to an overnight news event, Delta hedging will not save you. Gamma will have warped your Delta so severely during the crash that your stock hedge will be completely incorrect.

Step 3: Delta-Gamma Hedging

To protect against large, sudden moves, traders execute Delta-Gamma Hedging.

You cannot hedge Gamma by buying or selling the underlying stock, because the stock’s Gamma is exactly 0. (A share of stock always has a Delta of 1.0; its speed never changes, so its acceleration is 0).

To hedge Gamma, you must use other options.

If a trader is heavily Short Gamma (because they sold a lot of ATM straddles), they must go into the market and buy other options (like cheap OTM calls and puts) to add positive Gamma to their portfolio, bringing the Net Gamma closer to 0.

Once their Gamma is neutralized, they re-balance their stock position to neutralize their Delta.

A portfolio that is both Delta-Neutral and Gamma-Neutral is immune to both small ticks and large swings in the underlying stock. It has been mathematically immunized against directional risk.

<br>

Chapter Summary

- The Greeks: A suite of risk metrics that measure an option’s theoretical price sensitivity to constantly moving variables (Stock Price, Time, Volatility, Rates).

- Delta (Δ): Measures price sensitivity to a $1 change in the stock. It acts as the option’s “speedometer,” dictates the exact hedge ratio for market makers, and serves as a rough proxy for the probability of expiring ITM.

- Gamma (Γ): Measures the rate of change of Delta. It is the “acceleration.” High Gamma means the option’s directional risk profile is changing rapidly.

- The Convexity Trade-off: Option buyers are Long Gamma (enjoying accelerating gains and decelerating losses), while option sellers are Short Gamma (forced to buy high and sell low to maintain a Delta-Neutral hedge).

- Delta-Gamma Hedging: Advanced risk management requires using the underlying stock to neutralize Delta, and using other options to neutralize Gamma, thereby immunizing the portfolio against both small and large directional price shocks.

<br>

Discussion Questions

- If you are a retail trader who just bought a single Call option as a speculative bet, do you care if you are “Delta-Neutral”? Why do market makers care so deeply about this concept while retail speculators do not?

- Assume you own an At-The-Money (ATM) Call option that expires in exactly two hours. Why would its Gamma be incredibly high compared to an option that expires in two years? (Think about the cliff-edge analogy).

- If a stock is currently trading at $100, and you own a deep In-The-Money Call option with a strike of $50, what is your approximate Delta, and what is your approximate Gamma?

Step-by-Step Exercise: The Impact of Gamma

Let’s see exactly how a high Gamma warps your Delta during a stock move.

The Setup:

- Current Stock Price: $50.00

- You own 1 Call Option Contract (100 shares).

- Current Option Premium: $3.00

- Current Delta: 0.50 (per share)

- Current Gamma: 0.10 (per share)

Scenario: The stock price suddenly shoots up from $50.00 to $52.00 (a $2.00 move).

Note: We are going to use a simple step-by-step approximation.

- Calculate the Delta Impact: Using only the original Delta, how much value would the option premium theoretically gain from a $2.00 stock move?

- Calculate the New Delta: The stock moved $2.00. Gamma tells you how much Delta changes per $1 move. What is the exact new Delta of your option after this $2.00 move?

- The Gamma Reality: Because your Delta was accelerating during the move (growing from 0.50 toward its new value), your actual option profit will be higher than what you calculated in Step 1. This “bonus” profit is the financial reward of being Long Gamma!

(By calculating the shifting Delta, you can clearly see how static models fail during explosive market moves.)